Why this category matters

Portfolio intelligence is becoming an infrastructure question. The relevant issue is not whether a system can generate more outputs, but whether it can govern portfolio behavior when market conditions change.

Network-aware portfolio intelligence ecosystem. Reads the portfolio as one living system and is designed to stay disciplined when market conditions change. Built around selection quality, relationship quality, exposure quality, stress behavior and governance.

Professional conversations only when fit is clear. The current priority is internal capital deployment, live-system refinement and structured evidence accumulation. Strategic discussions remain case by case.

The market does not need another signal layer. It needs governed portfolio intelligence that can read relationships, reject fragility and keep capital decisions coherent when regimes change.

THE SIGNAL TRAP

The longer capital sits in a position, the more time drift has to accumulate.

Medium-horizon discipline: long enough to filter short-term noise, short enough to keep capital responsive when market conditions change.

Quantic Eagle is not another signal model. It is a governed portfolio intelligence ecosystem built around selection quality, network behavior, stress response and capital discipline.

THE PIPELINE QUESTION

The model is not the moat. The pipeline is.

The ecosystem approach: governed, repeatable and built around disciplined rejection. Many candidates can be generated. Only a small subset should ever deserve capital.

A disciplined governance loop for capital decisions under changing regimes: selection, exposure, risk, restraint and monitoring inside one coherent portfolio ecosystem.

One rule: if behavior is not coherent, it does not deserve capital.

Internal snapshot (selection phase): KPIs and equity curve.

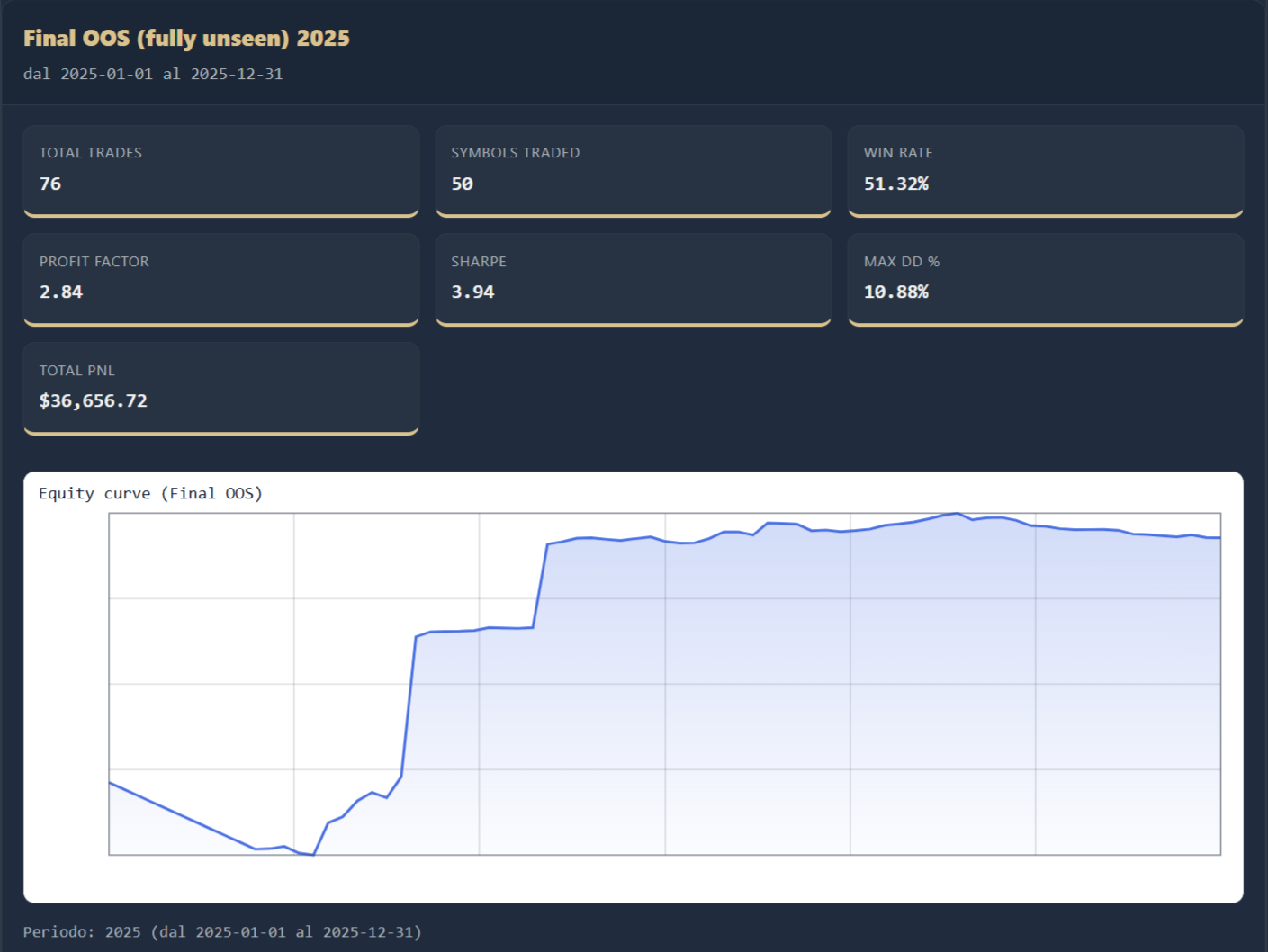

Final review on market data not used during development: KPIs and equity curve.

Stress regime snapshot: KPIs and equity curve.

Internal research snapshots with consistent assumptions. Shared to explain the evidence discipline, not to imply future results.

A serious conversation can explore observable behavior and risk discipline without exposing the proprietary architecture underneath.

When there is a serious professional reason to engage, the conversation can cover observable behavior, risk discipline, portfolio-level monitoring and the evidence process without disclosing proprietary internals.

Institutional and professional counterparties, prop and systematic boutiques, and strategic partners aligned with this operating model.

This page is designed for qualified counterparties who want to understand the category, the architecture and the review perimeter without receiving access to proprietary internals.

Portfolio intelligence is becoming an infrastructure question. The relevant issue is not whether a system can generate more outputs, but whether it can govern portfolio behavior when market conditions change.

A proprietary portfolio intelligence ecosystem for liquid markets, designed to evaluate relationships, filter candidates, monitor stress behavior and support disciplined capital decisions.

Family offices, strategic investors, systematic teams, technology-led financial groups, potential acquirers and institutional counterparties exploring portfolio intelligence as strategic infrastructure.

Only when the thesis, the operating architecture and the strategic value of governed portfolio intelligence are relevant to the counterparty.

When there is a serious reason to engage, the conversation can move from thesis to observable behavior: risk discipline, portfolio-level monitoring, structured evidence and how the system behaves when market conditions change.

Conversation context

Use this form only if there is a serious institutional, strategic or infrastructure-level reason to contact Quantic Eagle. The message can be short. If the reason is relevant, the conversation can continue privately.

Share the reason for the conversation. Keep it direct. If the context is relevant, Quantic Eagle may continue the discussion privately.

Quick clarifications for institutional evaluation and monitoring discussions.

It means a governed ecosystem for portfolio decisions: research discipline, candidate selection, risk boundaries, exposure control, internal execution logic and monitoring outputs inside one coherent operating loop.

The architecture connects research discipline, repeatable validation, portfolio-level risk controls, internal decision logic and monitoring telemetry under one operating system. The objective is not to create more signals. The objective is to decide what deserves capital, what should be constrained and what should be rejected.

Proprietary internals remain protected. Professional review, when relevant, can cover observable behavior, risk discipline and monitoring outputs without disclosing code, model weights or internal decision logic.

Signal generators often focus on directional calls. A portfolio control system focuses on decisions under uncertainty: how large positions are, what constraints apply, what risk budget is being used, how positions are managed/exited, and how behavior is monitored as conditions drift.

A simple illustration:

A professional context can cover observable behavior, risk discipline, portfolio-level monitoring and structured evidence. It does not include execution access, system integration, model export, proprietary code or model weights.

When there is a serious reason to engage, the conversation can move from thesis to observable behavior: risk discipline, portfolio-level monitoring, structured evidence and how the system behaves when market conditions change.

Professional conversations are designed around clear intellectual property boundaries. Observable behavior can be discussed without transferring proprietary internals. No code, no weights, no model export and no system integration are provided through the public site.

A regime shift is a structural change in market conditions—volatility, correlations, and liquidity can change quickly—making behaviors calibrated on a different period degrade. The system is designed to remain governable as regimes change.

Silent degradation is gradual drift over time: exposures creep, correlations flip, liquidity changes, and a system can keep trading "as if nothing changed" until the problem becomes visible (e.g., drawdown). Monitoring is designed to surface it earlier.

The system is built around a medium-horizon, liquidity-aware discipline. The aim is to stay far enough from short-term noise while avoiding passive exposure through full regime changes.

For professional evaluation, the important point is not trade frequency. It is whether capital remains liquid, risk remains governed and the portfolio logic can adapt when the network changes.

It targets silent degradation with monitoring-first design, out-of-sample validation discipline, and stress-regime behavior checks. The intent is repeatability across asset universes and more audit-style, repeatable review—scaling coverage without scaling headcount one-to-one.

No. Quantic Eagle develops proprietary portfolio intelligence infrastructure and internal systematic research. We do not provide retail services, financial advisory, or third-party portfolio management.

This page is informational only. Not an offer. Not investment advice.

Because risk does not travel one position at a time. Correlations, exposures, and sensitivities shift across the portfolio before the effect becomes obvious in P&L. A 100-asset book contains 4,950 unique pairwise relationships, 9,900 directed cross-asset relationships, and 10,000 matrix cells when self-relations are included. Any one of those relationships can shift during a regime change.

Quantic Eagle is designed to monitor those relationships continuously — not only isolated signals. When two positions that moved independently start tightening, the system detects the change in the structure, not just the change in the price. This is the difference between monitoring positions and monitoring the network between them.